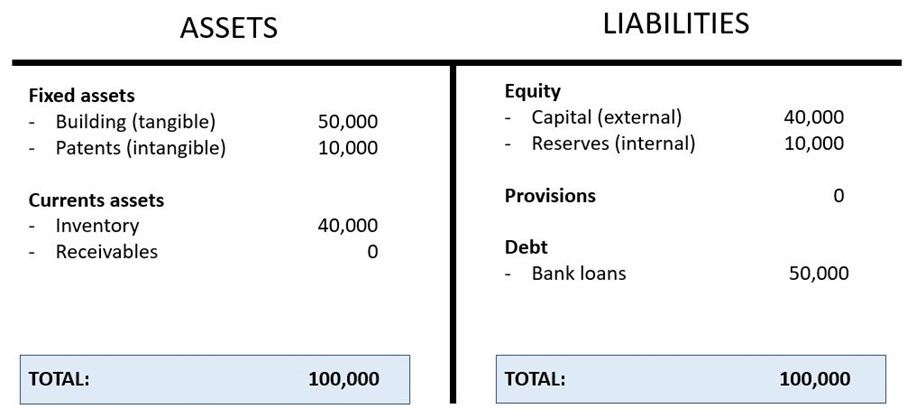

Cash and profit are two different things, let’s explain it with an example. A company has fixed assets for 60,000 EUR and an inventory equivalent to 40,000 EUR. It’s paid for by equity and bank loans.

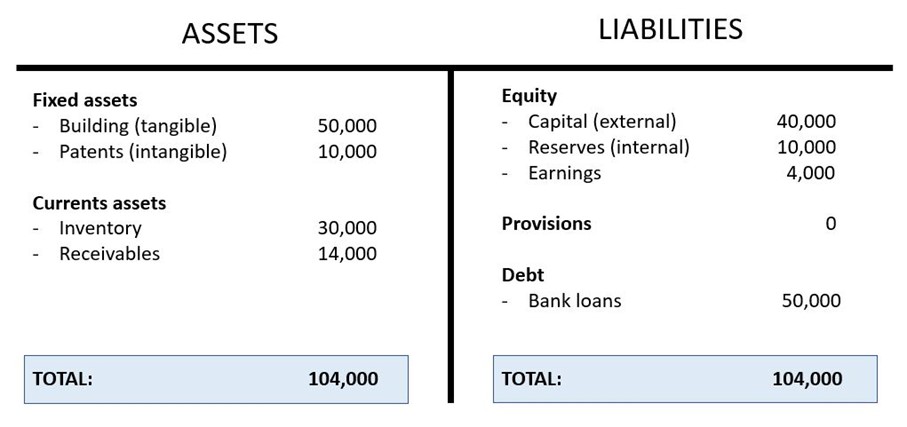

The company sells 10,000 EUR from the inventory for a sales price of 14,000 EUR. The company sends an invoice to the client, the latter has not yet paid. It changes the balance sheet:

After the sales an inventory of 30,000 EUR remains and the company has sent an invoice of 14,000 EUR which is booked as a receivable. The invoice has not yet been paid so there is no cash flow.

Even if the invoice hasn’t been paid, a sale has been made so there is a profit.

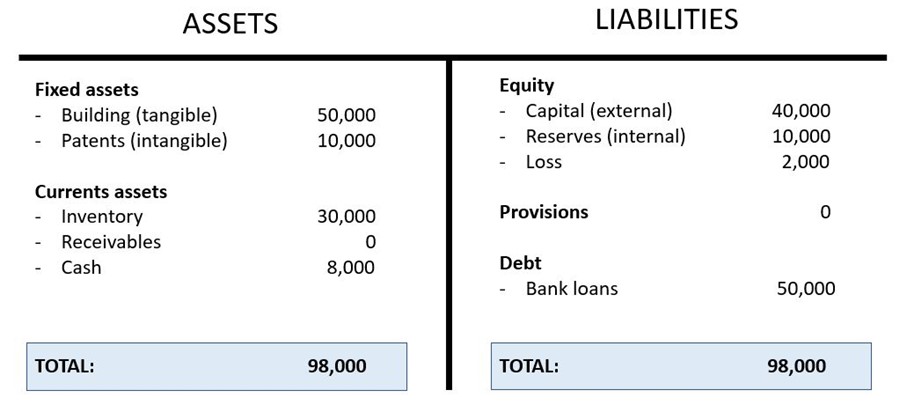

Imagine the same company and the same situation, with only one difference: the goods are sold for 8,000 EUR, causing a loss of 2,000 EUR. The sales price is paid immediately:

The inventory decreases by 10,000 EUR, as the sale is paid immediately the money is on the bank account and there are no receivables.

On the liabilities side, equity is decreasing with the loss of 2,000 EUR.

The balance sheet diminished from 100,000 EUR to 98,000 EUR.

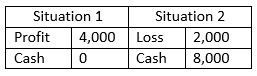

We can conclude that:

A company can have a profit and still have cash problems.

A company can have a loss and no cash problems.

Of course, a healthy company has both profit and cash.

Bankruptcy A bankruptcy has a very simple cause: the company cannot pay its creditors (such as banks, personnel and suppliers) anymore and is unable to convince any investors to put more money into the company. So bankruptcy has everything to do with cash problems. This means that loss making companies can continue to do business as long as there still is cash. Making a loss means that the company’s activities cost more than they generate. As long as these negative internal resources are compensated by external money (equity or debt) or savings (e.g. on the bank account) there are no cash problems and the company will not go bankrupt.